At Bernstein’s India Innovators Conference 2026, Sona BLW Precision Forgings laid out a single thesis: the same building blocks that power next-generation mobility can power Physical AI, from driveline to humanoids. The numbers back the story: roughly half of sales now come from outside India, BEV is a third of auto product revenue, and the company has already printed a record quarter above ₹1,200 crore in revenue. Here is what that pivot means for Sona BLW revenue, Physical AI, and automotive robotics supply chains.

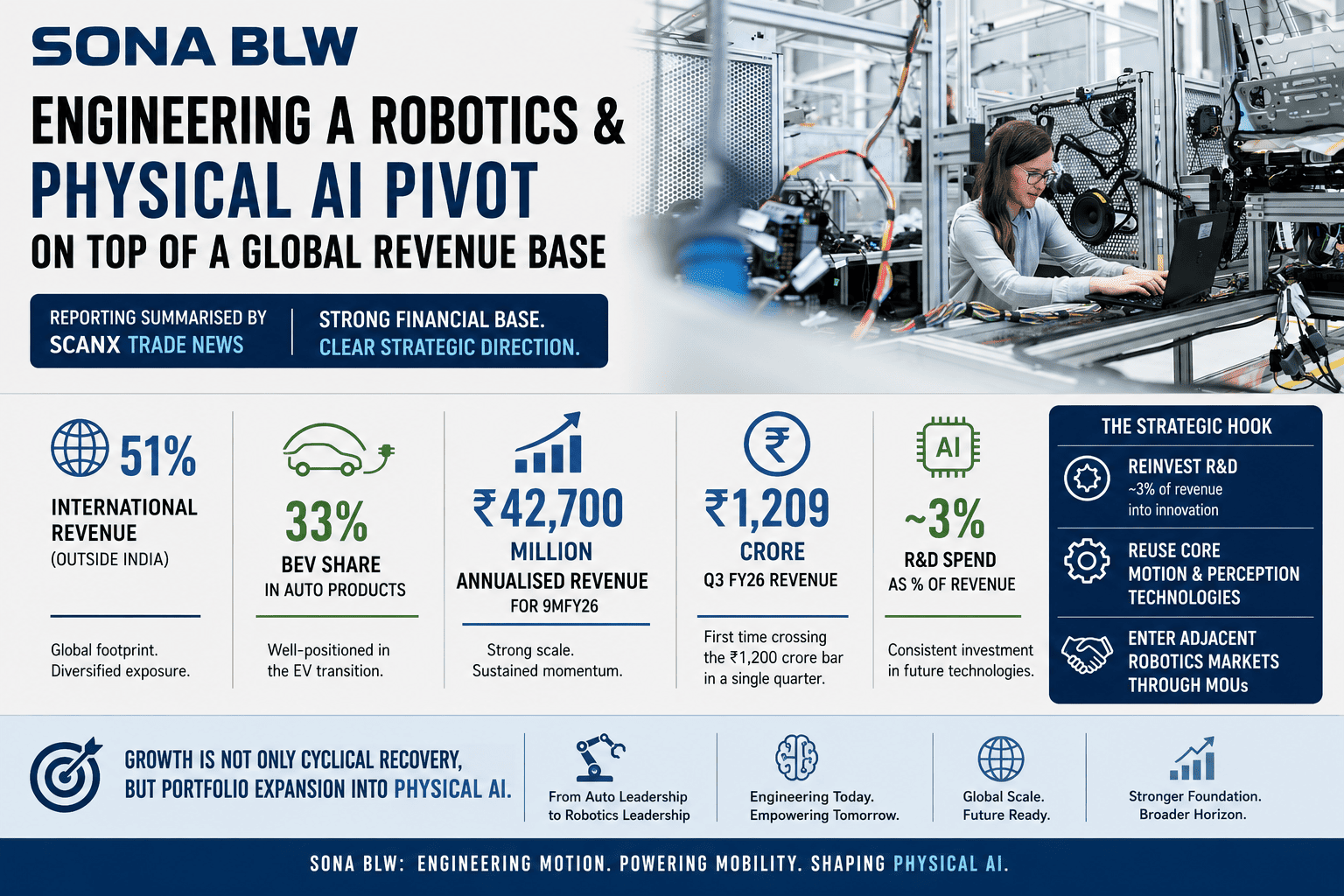

Sona BLW is engineering a robotics and Physical AI pivot on top of an already-global revenue base. Reporting summarised by ScanX Trade News ties the Bernstein presentation to 51% international revenue (outside India), 33% BEV share in auto products, and ₹42,700 million annualised revenue for 9MFY26, while separate ScanX coverage of Q3 FY26 highlights ₹1,209 crore quarterly revenue, the first time the company crossed the ₹1,200 crore bar in one quarter. The strategic hook is simple: reinvest R&D (about 3% of revenue), reuse core motion and perception technologies, and enter adjacent robotics markets through MoUs, so growth is not only cyclical recovery but portfolio expansion into Physical AI.

The 51% international revenue figure is not a vanity metric, it is a structural proof of what happens when an Indian precision manufacturer invests consistently in global quality standards, customer proximity, and technology differentiation over a decade. For suppliers watching this trajectory, the implication is clear: international revenue at scale requires verified partnerships and market access infrastructure built years before the revenue arrives, not after it is needed.

According to ScanX, Sona BLW presented at Bernstein’s India Innovators Conference on 12 March 2026, filing its investor deck with exchanges under SEBI norms. The framing is deliberately cross-industry: Physical AI, intelligent systems that sense, decide, and move in the real world, sits beside EPIC Mobility (Electric, Personalized, Intelligent, Connected) as the company’s umbrella for growth beyond traditional driveline components.

“The Future Can’t Wait”, the conference title, is a fair summary of why auto suppliers with motion, power, and perception IP are racing to claim robotics adjacencies before product cycles lock in.— Context from Bernstein India Innovators Conference 2026 coverage (ScanX Trade News)

The EPIC Mobility framework, Electric, Personalized, Intelligent, Connected, is Sona BLW’s way of describing a vehicle architecture shift that is already underway across its major OEM customers. But the move to Physical AI extends that thesis: if the company has already built the engineering competence to handle electric motors, torque-optimised gearboxes, battery management electronics, and sensor fusion for vehicles, those same competencies are the enabling technology for the next generation of warehouse robots, surgical assistants, industrial AMRs, and humanoid platforms. The Bernstein presentation crystallises this not as a future aspiration but as a current engineering reality, with MoUs, a CES demo, and a functioning R&D organisation already pointed at non-vehicle applications.

Think of Physical AI as software-defined behaviour with electro-mechanical consequences: the same competencies that let a vehicle manage torque, thermal limits, and sensor fusion can transfer to automotive robotics platforms, AMRs, industrial arms, and humanoids, where safety, precision, and power density matter just as they do on the road. The strategic insight is that the intellectual property required to build a competitive EV driveline module and the intellectual property required to build a competitive robotic actuator overlap substantially. That overlap is the basis of Sona BLW’s diversification thesis, and the reason the pivot is credible rather than speculative.

The conference timing is also relevant context. Bernstein’s India Innovators event sits at the intersection of institutional equity analysis and corporate strategy disclosure, attendees include fund managers and analysts who will stress-test the robotics narrative against financial projections. The fact that Sona BLW chose this venue to present the Physical AI thesis, and filed the materials with exchanges simultaneously, signals that the management team is prepared to be held accountable to the trajectory they have described. That accountability posture, combined with the actual financial performance in Q3 FY26, is why the market is taking the robotics pivot seriously rather than dismissing it as investor relations packaging.

EPIC Mobility is not just a branding exercise. It describes the architectural shift from mechanical to software-mechanical vehicles, and the supplier ecosystem that shift creates. Tier-1 and Tier-2 suppliers that can deliver at the software-mechanical boundary (actuators with embedded intelligence, sensors with onboard processing, gearboxes with real-time torque adaptation) are positioned differently from suppliers who can only deliver passive mechanical parts. Sona BLW’s 3% R&D investment, 500 R&D staff, and 133 patents are the infrastructure for competing at that boundary. The Physical AI pivot is the natural extension of that positioning into non-vehicle markets.

ScanX’s summary of the Bernstein presentation lists five technology pillars the company treats as common between advanced vehicles and robotics. Understanding each layer helps clarify why the automotive-to-robotics transition is less of a leap than it appears from the outside, and why the 3% R&D investment compounds across both markets simultaneously.

Lightweight, efficient motion at the heart of both BEV drivetrains and robotic joint actuators. Sona BLW’s precision manufacturing background in gears and differential assemblies translates directly into high-torque-density motor integration, the kind of actuation performance that determines range and responsiveness in electric vehicles and determines dexterity and cycle speed in robotic systems. The engineering discipline is identical; only the application geometry changes.

Torque conversion with precision manufacturing know-how, the foundational competency that Sona BLW was built on. Modern robotics platforms require gear trains with tight tolerance, low backlash, and reliable thermal management across millions of cycles. These are exactly the requirements automotive transmission suppliers meet under the harsh conditions of vehicle service life. The CES 2026 eVTOL gearbox showcase was a direct demonstration of this transfer, the same precision that goes into a passenger car differential, now going into a vertical-takeoff aircraft drivetrain.

Energy storage and delivery for extended runtimes, the layer that determines operational duration in both EVs and autonomous mobile robots. Power electronics design for automotive-grade reliability (vibration, thermal cycling, humidity) is significantly more demanding than consumer electronics design, which means automotive power electronics suppliers are over-spec for most industrial robotics environments. This creates a built-in quality advantage when transitioning to robotics customers who have industrial, not consumer, reliability expectations.

Camera, radar, LiDAR, and ultrasonic modalities, the sensory layer that enables both ADAS in vehicles and navigation, mapping, and collision avoidance in robotics platforms. The sensor fusion algorithms, calibration methodologies, and physical packaging requirements overlap substantially between a vehicle-mounted sensor array and a mobile robot sensor suite. A supplier with automotive-grade sensor integration experience arrives at the robotics market with a testing rigour and integration methodology that most robotics-native startups lack.

Real-time decision-making at the edge, the intelligence layer that transforms a collection of motion, power, and sensing hardware into an autonomous system. Sona BLW’s 125 software engineers within a 500-person R&D organisation represents a meaningful investment in this layer. Edge AI for automotive applications must meet functional safety standards (ISO 26262), latency requirements, and power constraints that are equally applicable to safety-critical robotics deployments. The 133 patents cited in presentation materials span this entire stack, not just the mechanical components.

If those five layers are real manufacturing strengths, not slideware, then automotive robotics becomes a segment extension, not a moonshot. That is the core investment logic behind the pivot: amortise R&D and capex across more end markets while Sona BLW revenue scales with both EV programmes and non-auto verticals (rail, off-highway, industrial, and now Physical AI). The company is not changing what it knows how to do, it is changing who it sells that capability to, expanding the addressable market dramatically without expanding the engineering risk proportionally.

ScanX lists several concrete moves that connect the strategy to products and demos. Each partnership signals a different dimension of the Physical AI expansion, humanoids, aerial mobility, premium EV systems, and public demonstrations at the world’s most visible technology trade show.

| Initiative | Focus | Why It Fits Physical AI | Status (ScanX) |

|---|---|---|---|

| Neura Robotics MoU | Humanoid robot product development | Transfers precision motion and systems integration skills into bipedal platforms, the hardest actuation problem in robotics | MoU signed |

| The ePlane Company MoU | eVTOL development | Extends powertrain and lightweight mechanical expertise into aerial mobility, weight, reliability, and noise disciplines that directly overlap with EV subsystems | MoU signed |

| ClearMotion collaboration | Active suspension for Nio ET9 | Shows tier-1 ability in software-mechanical boundary systems for premium EVs, active suspension is precisely a Physical AI application: real-time actuation driven by onboard intelligence | In production |

| CES 2026 | AMR platform & eVTOL gearbox showcase | Signals to global OEMs and robotics buyers that IP is demo-ready, not conceptual, CES is where automotive and consumer electronics procurement teams validate supplier technical readiness | Demoed Jan 2026 |

An MoU toward humanoid development is a high-ambiguity, high-upside bet: success depends on joint roadmaps, safety certification paths, and clear IP boundaries, the same partnership mechanics GTsetu helps teams structure early. Neura Robotics is a German humanoid robotics company that has raised significant venture capital for commercially deployed humanoids. The partnership gives Sona BLW a direct development relationship with one of the most credible humanoid programmes globally outside of the US market.

Electric aircraft stress weight, reliability, and noise, disciplines that overlap with automotive EV subsystems and gearbox engineering. The ePlane Company is an IIT Madras spin-out developing electric aircraft for the Indian urban air mobility market. For Sona BLW, this is both a technology partnership and a market positioning signal: the same engineering team that builds aircraft gearboxes builds passenger car gearboxes, and that dual-domain credibility matters increasingly as aerospace procurement teams evaluate automotive-grade suppliers for aerial mobility programmes.

The ClearMotion active suspension collaboration for the Nio ET9 is the most immediately revenue-relevant partnership in the Physical AI portfolio. Active suspension is a real-time actuated system driven by onboard computing, precisely the software-mechanical boundary that the Physical AI thesis describes. Shipping this system on one of China’s most premium electric vehicles validates that the company can operate at the intersection of hardware precision and software intelligence at OEM production standards.

An MoU is a door, not a deal. The Neura Robotics and ePlane Company MoUs signal intent and open engineering dialogue, but the value is realised only if both parties follow through with structured roadmap alignment, clear IP ownership agreements, joint development milestones, and defined exit conditions. The companies that convert MoUs into revenue are the ones that formalise the collaboration structure before technical work begins, not after a prototype is built and both parties are arguing about who owns the output. GTsetu’s NDA-first workflow and collaboration framework exist precisely to prevent that common failure mode.

Scale still lives in factories and labs. ScanX notes 12 manufacturing plants across 5 countries, 5 R&D centres, and 3 engineering capability centres, with 500 R&D employees including 125 software engineers. That footprint is what makes a 51% international revenue number believable: it reflects installed capacity and customer proximity, not accounting tricks.

The international footprint deserves more than a percentage headline. Building to 51% international revenue from an Indian base requires years of quality system investment (IATF 16949 certifications and customer-specific quality approvals from global OEMs), proximity manufacturing in customer geographies (hence plants across five countries, not just India), and the kind of engineering talent that can hold a technical conversation with a Tier-0 OEM’s development team in Germany, the US, or China. Sona BLW has built all three. That infrastructure is not replicable quickly by competitors, it is the structural barrier that protects the revenue mix from erosion even as the company expands into new Physical AI markets.

The railway vertical, included among the four revenue segments, is an important signal about how the company thinks about technology leverage. Railway propulsion and traction systems share mechanical and power electronics disciplines with automotive drivetrains, but serve a market with longer product cycles, stricter safety certifications, and less price pressure. Moving into railway is the same IP-leverage play as moving into robotics: use the same engineering base to serve a higher-value, more stable market segment alongside the core automotive business. The 31% non-automotive share in 9MFY26 suggests that leverage is already working at material scale.

Humanoid and eVTOL OEMs are geographically concentrated today, primarily in the US, Germany, and China for humanoids; India, Europe, and the US for eVTOL. A supplier with manufacturing presence in five countries and engineering capability centres that span geographies is structurally better positioned to win Physical AI supply contracts than an India-only manufacturer, regardless of technical capability. Regulatory certification, local content requirements, and customer supply chain risk policies all favour suppliers with local manufacturing options. Sona BLW’s multi-country footprint, built for automotive customers, becomes a differentiator when pitching to robotics and aerial mobility OEMs as well.

Sona BLW’s story is a case study in technology leverage: reuse motion, power, and perception stacks; enter robotics and mobility adjacencies through MoUs and structured collaboration; keep scaling Sona BLW revenue with a global customer mix. For suppliers and OEMs evaluating similar moves, the bottleneck is rarely ambition, it is finding the right verified partners across borders without burning six months on dead-end conversations and unverified capability claims.

The partnership pattern Sona BLW has followed, start with technology dialogue, formalise via MoU, invest jointly in specific programmes, is the cleanest path for any manufacturer entering an adjacent market with existing IP. The risk points are also predictable: IP ownership ambiguity, capability verification failures (your partner claimed capability X and delivered capability X-minus), and governance gaps that cause decision-making paralysis when a product development choice needs to be made quickly. Addressing all three of those risk points before the first engineering conversation begins is the difference between partnerships that generate revenue and partnerships that generate legal costs.

| What Sona BLW Did | Why It Worked | How GTsetu Enables This for Your Company |

|---|---|---|

| Invested consistently in R&D (3% of revenue) across both automotive and non-automotive IP | IP depth is the foundation for all partnership discussions, without it, you are a contract manufacturer, not a technology collaborator | ✓ GTsetu helps you find partners who bring complementary IP you don’t already have, the discovery process starts with capability gap identification |

| Formalised partnerships via MoU before beginning joint development work | Structural clarity upfront prevents IP disputes, governance conflicts, and misaligned expectations that kill partnerships after the engineering work is done | ✓ Built-in NDA and collaboration workflow, share nothing sensitive until agreements are in place, with a full audit trail from first contact |

| Chose partners with complementary capabilities, not overlapping ones (Neura brings humanoid software and design; Sona BLW brings actuation and precision manufacturing) | Partnership value comes from capability gaps, each party should be delivering something the other cannot efficiently build alone | ✓ Detailed capability profiles help identify complementarity, browse verified partners whose strengths fill your gaps before you reveal your roadmap |

| Built multi-country manufacturing presence over years, making “international” revenue structural rather than cyclical | Geographic customer proximity reduces supply chain risk, satisfies local content requirements, and enables faster programme support, all of which improve win rates with demanding OEMs | ✓ GTsetu’s 100+ country network includes local manufacturing and distribution partners in every major automotive and robotics market globally |

| Demoed at CES 2026 to validate readiness with global procurement audiences | Credibility with new customer segments requires proof, not promises, early demos compress the trust-building timeline with buyers who have no prior experience with the supplier | ✓ Anonymous discovery means you can evaluate partner credibility before they know you are evaluating them, reducing the time wasted on partners who cannot actually deliver |

Figures and conference references in this article follow ScanX Trade News coverage of Sona BLW Precision Forgings at Bernstein Innovators Conference 2026, with additional quarterly metrics from ScanX’s Q3 FY26 results coverage. Always cross-check with official exchange filings before making investment decisions. The analysis in this article is editorial commentary based on publicly reported figures, not investment advice.

If your roadmap looks like Sona BLW’s, global revenue, robotics adjacencies, and deep motion stack IP, GTsetu helps you discover verified manufacturing and technology partners across 100+ countries, with NDA protection built in from day one. Zero broker fees. Anonymous discovery until you are ready to engage. 6-point government-sourced identity verification on every company in the network.

Find verified partners free → Browse the network

Business Development Expert | Global Trade & Cross-Border Partnerships

Lui Wang is a Business Development Expert at GTsetu, specializing in international trade, cross-border partnerships, and market expansion strategies. With extensive experience working across diverse business ecosystems, Lui helps companies identify growth opportunities, establish strategic collaborations, and navigate the complexities of global commerce.

His expertise spans manufacturing, supply chain partnerships, technology collaborations, market entry strategies, and international business development. Through GTsetu, Lui works closely with businesses, trade organizations, and industry stakeholders to facilitate meaningful connections that drive sustainable growth across regions and sectors.

Lui is particularly passionate about helping organizations build long-term international partnerships, unlock new markets, and strengthen their global competitiveness in an increasingly interconnected economy.