When a US technology giant deliberately moves Apple Manufacturing India toward roughly one-quarter of global iPhone output, the signal is bigger than tariffs alone: it is a structural bet on a dual-hub iPhone supply chain, government-backed scale-up, and a consumer market growing fast enough to justify double-digit revenue expansion on the ground. Whalesbook Industrial traces how Foxconn expansion alongside Tata Electronics and Pegatron is turning India into Apple’s second gravity well, with Vietnam still in the mix for other lines.

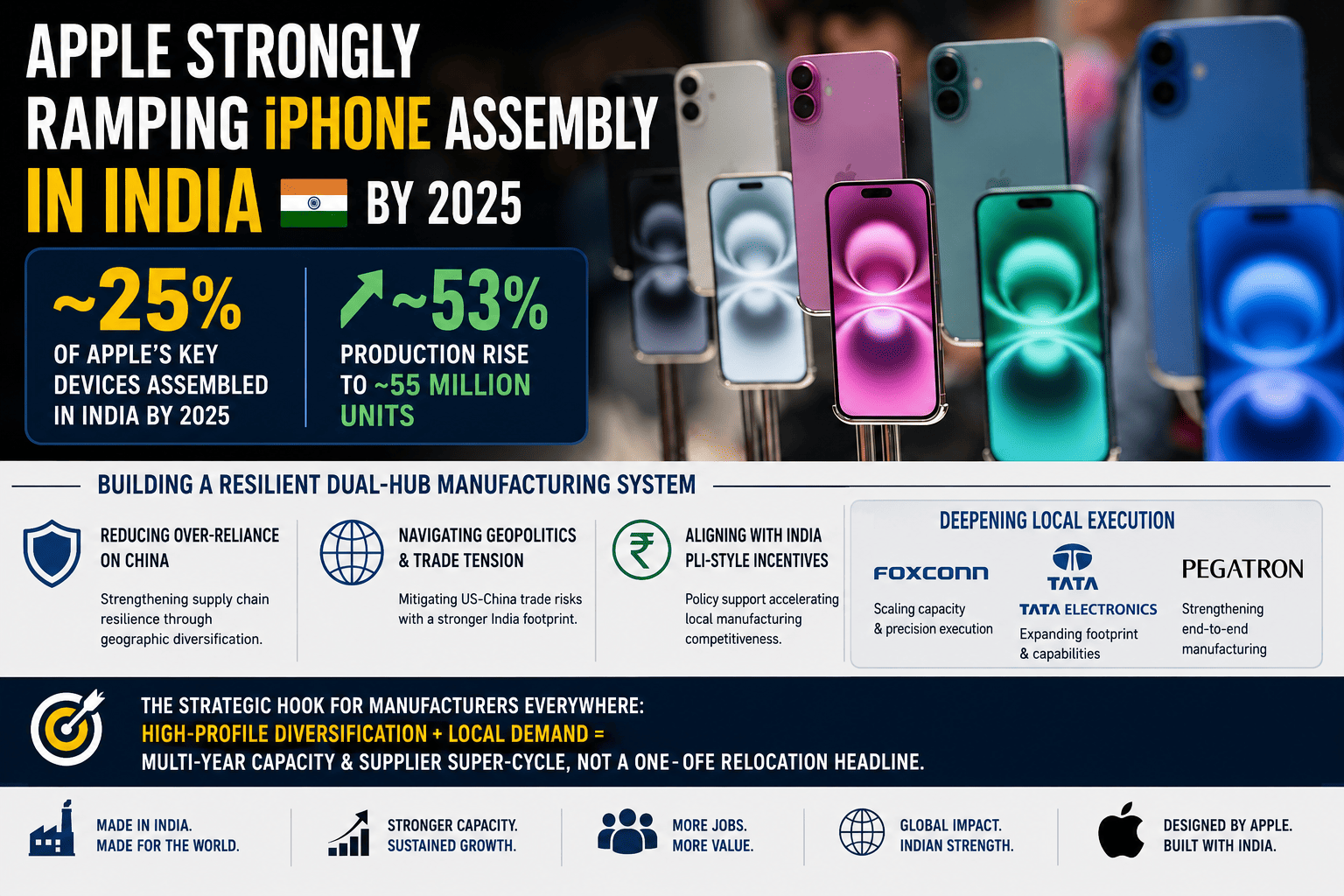

Per Whalesbook Industrial, Apple has significantly ramped iPhone assembly in India: by 2025 the country accounted for about 25% of Apple’s key devices, with production rising roughly 53% to ~55 million units. The story is framed as a resilient dual-hub manufacturing system, reducing over-reliance on China, navigating geopolitics and US-China trade tension, and aligning with India PLI-style incentives, while Foxconn, Tata Electronics, and Pegatron deepen local execution. The strategic hook for manufacturers everywhere: high-profile diversification plus local demand can compound into a multi-year capacity and supplier super-cycle, not a one-off relocation headline.

The iPhone supply chain has historically been optimised for speed, labour depth, and component density in Greater China. Whalesbook describes Apple’s response as building a strong dual-hub system, moving beyond short-term tariff firefighting toward a proactive resilience posture. India becomes the clearest second pole for final assembly at scale; Vietnam plays a complementary role for selected categories where logistics and trade arrangements fit.

India is cementing its role as a vital complementary hub, not an overnight full replacement for China’s scale, but a parallel engine for growth and geopolitical balance.— Paraphrased synthesis of Whalesbook’s “India: A Key Complement to China” section

When a flagship OEM shifts Apple Manufacturing India into double-digit share of global output, tier-2 and tier-3 suppliers face a forced portfolio decision: qualify for India lines, invest in local content, or risk share loss on the world’s highest-volume premium handset stack. That is the global shift your hook points to, diversification as default, not optional optimisation.

Whalesbook explicitly names Foxconn alongside Tata Electronics and Pegatron as partners strengthening assembly and supplier relationships in India. For anyone mapping Foxconn expansion, the takeaway is operational: Apple’s India super-cycle runs through contract manufacturers and integrators who can hit quality, traceability, and ramp curves, the same pattern that defines modern iPhone supply chain governance globally.

| Partner role (per Whalesbook) | Strategic function | Implication |

|---|---|---|

| Foxconn (Hon Hai) | Scale EMS / assembly depth | Primary lever for line transfers and capex-heavy fabs-adjacent integration |

| Tata Electronics | Domestic industrial champion in Apple’s India stack | Local credibility, policy navigation, long-horizon manufacturing investment |

| Pegatron | Additional EMS capacity | Supplier diversification inside India, reduces single-site concentration risk |

Whalesbook notes India’s electronics sector growth over the last decade, driven heavily by mobile production, with forecasts that national electronics output could exceed $610 billion by 2030, context for why Apple-scale anchors matter for the whole cluster.

Apple also produces categories such as AirPods and MacBooks in Vietnam, efficient logistics and trade arrangements are cited as advantages, illustrating a multi-node Asia strategy rather than India-only reshoring.

Whalesbook ties Apple’s acceleration to US-China trade tensions and tariff pressure while noting India’s Production Linked Incentive (PLI) schemes as a partial offset to higher costs versus China or Vietnam. The article also flags that manufacturing costs in India can remain higher, and that policy continuity matters, including discussion of PLI timelines and possible extensions or successor frameworks as of early 2026 commentary in the piece.

Whalesbook frames the India expansion partly as tariff arbitrage, moving production to a geography with better US trade optics. The dual-hub strategy de-risks the supply chain against further escalation in US-China policy friction.

Strategic resilience driverIndia’s Production Linked Incentive scheme provides per-unit production benefits that partially offset the 11–14% cost disadvantage vs China. The catch: PLI schemes have timelines, and Whalesbook flags that extensions or successor frameworks are actively discussed as of early 2026.

Policy-dependent advantageApple’s India strategy is reinforced by strong domestic demand, double-digit revenue growth cited by Whalesbook. Manufacturing locally signals commitment to a market of 1.4 billion people where premium smartphone penetration is still rising, India-tailored retail and product strategy follows production.

Demand + supply compoundingWhalesbook’s hurdles section reminds readers that India’s ecosystem still faces infrastructure gaps, imported component dependence (including semiconductors sourced via China-linked trade), and a labour model that can require larger headcount than China’s for comparable output. Any supplier entering on Apple’s coattails should model 11–14% cost disadvantage scenarios alongside incentive benefits, not headline capacity alone.

| Hurdle | Whalesbook framing | Near-term trajectory |

|---|---|---|

| Component ecosystem depth | China still superior on density, speed, and cost for sub-assemblies | Improving, Apple pulling suppliers to localise |

| Semiconductor import exposure | High dependence on China-linked chip flows for near-term production | Structural risk, multi-year horizon to meaningful independence |

| PLI scheme continuity | Critical to closing 11–14% cost gap; expiry creates uncertainty for large capex commitments | Extension / successor framework actively discussed per Whalesbook |

| Labour model and headcount | India’s labour laws and workforce scaling require larger headcounts for equivalent China output | Manageable with right EMS partners; embedded in cost gap estimate |

| Infrastructure and logistics | Port capacity, road infrastructure, and cold-chain logistics gap vs Shenzhen-to-port model | Government infrastructure spending accelerating; multi-year close |

Apple’s India arc is a textbook case of OEM-led ecosystem migration: anchor EMS (including Foxconn expansion), pull in component suppliers, and let Apple Manufacturing India statistics convince the rest of the tier stack to follow. For mid-market manufacturers, the winning move is rarely solo greenfield, it is verified JV, CM, or tier-2 qualification inside the same industrial corridors Apple’s partners already validated.

The lesson is replicable across supply chains: when a flagship OEM commits production volume to a new geography at scale, it creates a parallel opportunity for Tier 2 and Tier 3 suppliers to co-locate, qualify, and capture the demand wave that follows. India’s electronics cluster is accelerating precisely because Apple’s assembly anchor gives suppliers the demand visibility to justify their own capex decisions. The question for any manufacturer watching this story is: what is your entry point into the corridors that Apple, Foxconn, and Tata Electronics are already validating?

This article summarises themes and figures attributed to Whalesbook, “Apple Ramps Up India iPhone Assembly to 25% of Devices” (Industrial / Goods & Services). Figures on stock price, valuation, and analyst targets in the original are time-stamped market commentary; verify against primary filings and your compliance policy before trading or allocating capital. Whalesbook includes an on-site disclaimer that some content may be AI-generated, triangulate with official Apple supplier disclosures and Indian regulatory releases where decisions depend on accuracy.

If Apple’s super-cycle is your market signal, GTsetu helps you find verified manufacturing and assembly partners across India and 100+ countries, NDA-protected from first technical touch. 500+ government-identity-verified companies. Anonymous discovery. Zero broker fees.

Business Development Expert | Global Trade & International Market Development

Sarah Ann Mitchell is a Business Development Expert at GTsetu with a strong focus on global trade, international market development, and strategic business partnerships. She works with companies seeking to expand internationally by identifying collaboration opportunities, connecting with key stakeholders, and developing market access strategies.

Sarah brings expertise in cross-border business development, international trade ecosystems, partnership building, and global market intelligence. Her work at GTsetu involves supporting businesses, manufacturers, startups, and industry leaders in building relationships that accelerate growth and create long-term commercial value.

Passionate about fostering international collaboration, Sarah helps organizations navigate evolving global markets and discover new opportunities through strategic partnerships, trade networks, and ecosystem-driven growth initiatives.